The General Case of Saroff's Rule

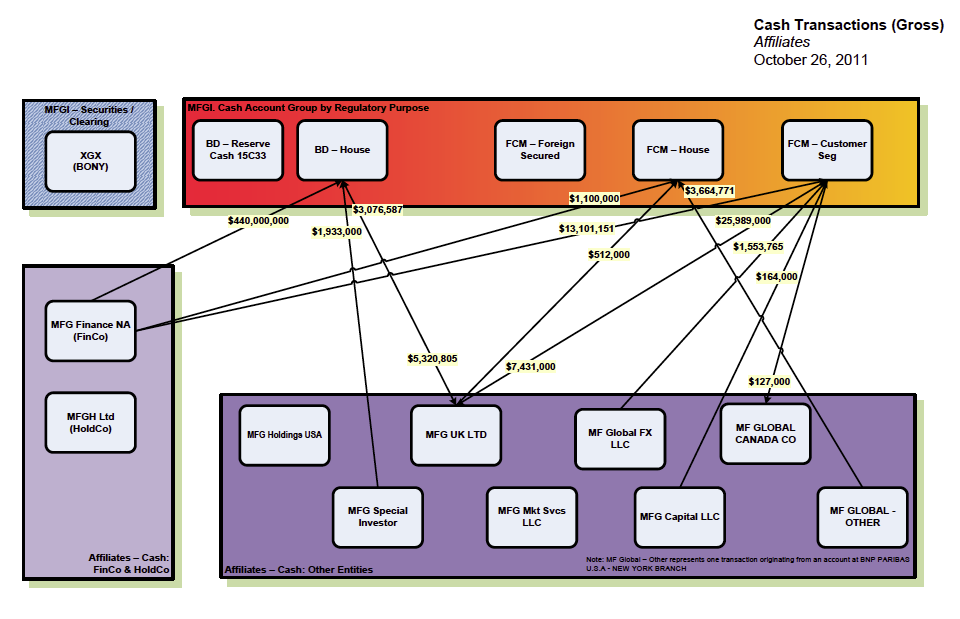

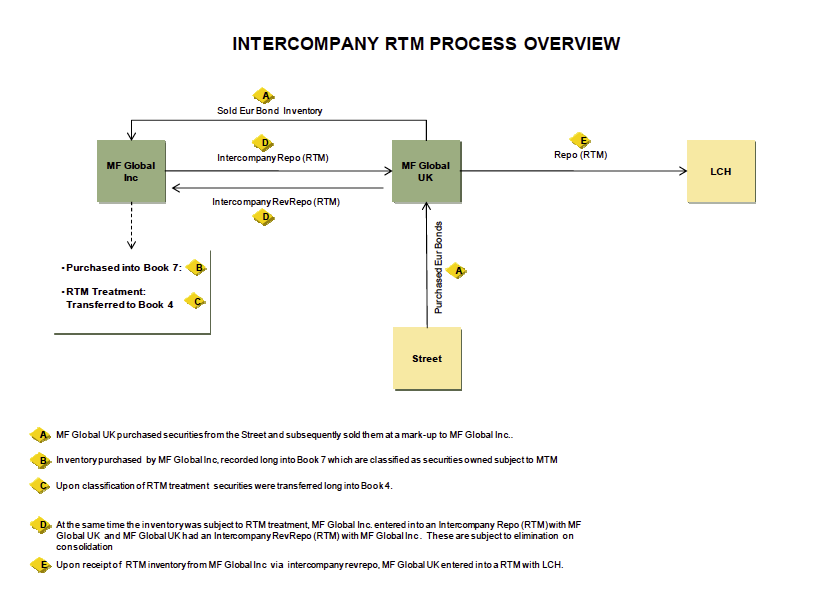

Let me remind you of what I call Saroff's Rule, "If a financial transaction is complex enough to require that a news organization use a cartoon to explain it, its purpose is to deceive."

Well, a recent paper by economists from MIT, ASU, and UCSD shows that complexity more generally appears to have deception as its primary purpose:

Economist George Akerlof has spent much of his celebrated career thinking about how trickery and deceit affect markets. His most famous insight, which won him the 2001 Nobel Prize in economics, is that when buyers and sellers have different information, lack of trust can cause markets to break down. In those models, no one actually ends up getting tricked -- everyone is perfectly rational, so even the possibility of getting cheated causes them to stay prudently out of the market. But in his book “Phishing for Phools,” written with fellow Nobelist Robert Shiller, Akerlof goes one step further. Much of the actual, real-world economy, he says, involves trickery and deception.I will go a step further than the economists do (45 page PDF), the words "fraud" "corruption" and "crime do not occur in the paper, and suggest that this complexity is present because of a deliberate and specific intent to deceive investors, and that the credit rating agencies were willfully blind to this because it made the money.

………

A recent paper by economists Andra Ghent, Walter Torous and Rossen Valkanov may shed some light on the question. Ghent and her co-authors look at mortgage-backed securities, which figured prominently in the crisis. They try to measure how complex various products were, using measures like the number of pages in the prospectus, the number of tranches in the security and the number of different types of collateral.

That allowed the researchers to see whether more complex products fared better or worse in the years before the crisis. Using Bloomberg data, they look at private-label, mortgage-backed securities issued between 1999 and 2007. They then look forward in time, to see which products defaulted and which ones experienced more foreclosures in the mortgage pools that they used as collateral.

It turns out that complexity was a bad sign. More complex deals experienced higher default rates and more foreclosures on their collateral. So if you were an MBS buyer from 1999 to 2007, the rational thing to do would have been to demand a higher interest rate on a more complex security.

Except that didn’t happen. Ghent et al. found that complexity had no correlation with the yields on MBS. That means that although more complex products were riskier on average, buyers didn’t recognize that fact. The authors also carefully exclude the possibility that complex deals commanded higher prices because they were specially tailored to individual buyers’ needs -- in fact, most products contained the same types of collateral, but the complex ones were just of lower quality.

………

Interestingly, Ghent and her coauthors find that credit-ratings companies tended to give higher grades to more complex products. That implied the credit raters were willing to trust issuers when figuring out what was actually in the products got too hard. Maybe it’s human nature to trust our counterparties more when things get too complicated. Or maybe the ratings companies’ well-known bad incentives took over when complexity and opacity made their misbehavior harder to observe.

To paraphrase Paul Volker, no useful innovations have come from banks since the introduction of the automatic teller machine.

Reinstate the principle you can only buy insurance on things when you have a direct interest in their continued existence.

It's a principle that was made law by the Marine Insurance Act of 1746, and worked until people decided that things like naked credit default swaps were an essential innovation.

Reinstate that.

Put derivatives at the back of the bankruptcy queue, not the front.

Put a Tobin tax on financial transactions.

Shut it down.

Shut it all down.